3 ways to keep the peace when you move in with your partner “too soon”

3 ways to keep the peace when you move in with your partner “too soon”

Shortly after Christmas, I moved in with my boyfriend. But it wasn't necessarily happening because we wanted it to. To make a long story short,... Read more

I moved in with my partner of two years about seven months ago. It’s my first time living with someone, at the not-so-tender age of in-my-thirties. The problem is that I have a Very Important need to pay my fair share of things we buy. Let’s call it a guilt complex stemming from who the hell knows what. Either way, when we started to share rent and utilities responsibilities, we had to figure out a way to make things equitable (with very different incomes), while also easing into the whole finance sharing idea in general.

This was, in all honesty, very scary for me. It’s scary to be helping to manage someone else’s money and attempting to be frugal when you’re the one using it (like for groceries, in my case — I do most of the food shopping). We decided on a “three pot” system of one shared account plus our own individual accounts. Here’s how we do it…

Our own accounts for non-shared items

Non-shared items such as clothing, toiletries, hobbies, etc. remain as paid from our own personal accounts. This means I’m not paying for his computer toys and he’s not paying for my tampons. It also means we can buy gifts for each other without anything suspicious hitting a shared account that the other could see.

Since we both have different incomes, we spend differently when it comes to things like meals. So we decided to keep dining out separately as a personal expense. That way if I’m being thrifty and living off of leftovers, he can grab a bite at work without having to worry about me paying for it. If we eat out together, we share the cost from the shared account.

One shared account for household expenses

We opened a joint bank account for shared household items, groceries, shared vacations, rent, split utilities, etc. We divided the rent according what we could pay and split the other utilities down the middle. Then we padded the number out for shared gift buying and other non-planned expenses.

We have to keep an eye out for overdrafts since we’re both pulling from this account, but otherwise it’s transparent and as equitable as it can be considering our income differences. There is some risk in having a shared account, especially when you’re not married. Don’t forget to learn what the risks entail in a joint account such as debt collection, credit damages, and tax issues.

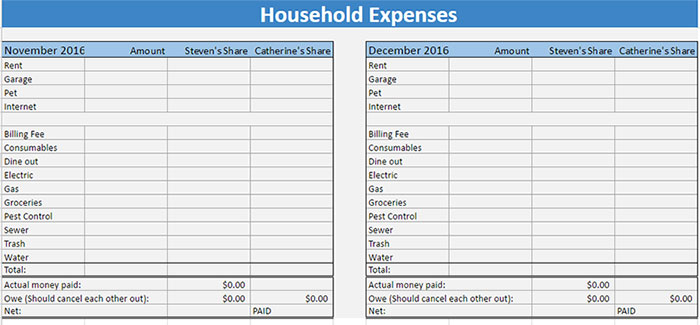

The big ol’ spreadsheet

Anyone at the Empire knows my love for a good spreadsheet (I made these for your wedding planning needs!), so naturally, we decided to keep track of the expenses with a monthly spreadsheet. We plug in the bills we pay, and it tallies up what we both owe (with different totals depending on your setup — say, if you pay a smaller percentage of the rent). It’s simple, but it gives us an overview of where we’re spending and on what.

It’s still scary to be putting money into a shared pot that becomes a nebulous thing, but it’s helping me (the worrier) to ease into the idea of sharing a life. It’s totally NOT mandatory to share any accounts with your partner, married or otherwise, but for us, this seems to be what works.

Next we’ll tackle how to manage the cats liking one of you over the other… just kidding.

About the Author: Catherine Clark

Catherine Clark loiters at her local library, makes art, watches movies en masse, plays video and tabletop games, poorly cooks healthy things, cuddles with her feline fur babies, and blogs at BijouxandBits.com.

“Next we’ll tackle how to manage the cats liking one of you over the other…”

You just need multiple cats, duh.

Now that’s my kind of solution!

We have the same system. It works really well. We also chat when we get paid about how our goals are going.

This is what my wife and I do and it really works for us. It gives transparency in the areas where we are already jointly financially responsible and but preserves each of our personal financial autonomy. I can’t see us ever doing it any other way.

Things that really helped us were monitoring the joint expenses and then working out a safe average and pre-paying that (plus small contingency, plus small contribution to holiday/house repairs pot) into the joint account each month. That basic pre-paid safe average is not split 50/50 for us but is proportionate to our individual incomes (the amount we pay is not the same but the proportion of income pretty much is).

As we have online banking we set up all the bill payments from the joint account as automatic, so we don’t have to keep discussing the fact I earn less than my wife (I am a perpetual student) and have done our entire relationship. This does my self-esteem a lot of good but the bills and the payment of them are totally transparent as I can access the statements anytime I want. We use a card attached the joint account for grocery shopping but eating out and also alcohol at the supermarket are negotiated extras which means we either split it from personal accounts or one of us treats the other, more usually my wife treats me (she’s a keeper!).

The other thing that really helps is having all these accounts at the same bank (money transfers between accounts at the same bank are instant in the UK) and even better if you can bank online. Our system is fairly hands off but every so often it needs checking and adjusting, it’s super convenient to do this at home on the laptop.

This is exactly what my husband and I did when we first moved in together. It was scary at first, but 10 years later and we still operate this way, except that a larger percentage of our money now goes into the joint account, and we use our personal accounts as more of an “allowance” to control frivolous spending. We made three rules in the beginning, and we’ve managed to stick by them:

1) We don’t make judgments or ask questions about the way the other person handles their personal account finances. (I tend to save and make larger purchases, whereas my husband loves spending his money on eating out and buying comic books.)

2) All joint account purchases must be discussed in some way.

3) We help each-other out, or make modifications to our allocations as necessary. (For example, my student loans don’t technically involve him, but we decided that it didn’t make sense for them to come out of my allowance.)

sounds perfect! I figure our shared account will grow in the same way. Thanks@!

My husband and I have a similar three-pot system except:

1. What we put into the joint accounts (a savings account to make sure we have money on hand for the property tax, a checking account for everything else) is based on the percentage of the household income we bring in. Right now we make roughly the same amount of money but when the split was 60/40, then the person making 60% paid 60% and the person making 40% paid 40%. Since my husband went on my health insurance, he’s paid an additional offset into the joint account and I’ve gotten a slight “cut” to make up for the fact that having premiums withheld for the family plan rather than the individual means less of my paycheck makes it home.

2. We more or less alternate paying out of our personal accounts for joint recreation like going out to dinner together. If necessary we’ll transfer personal money to each other if we’re paying for something big enough that it wouldn’t feel fair for one person to shoulder the expense. The joint account only gets used for discretionary spending if we do something like leave a portion of our tax refund in there for a trip together.

Hi there

Sounds like a great system! However, I’m wary of equating stuff like tampons to computer toys – one is a necessity like toilet paper, and the other sounds more optional. Generally I get those when we do the groceries, like I’d buy shaving cream, and they’re a shared expense, like birth control or pain killers. Idk, I guess I’m just wary of pink taxes and stuff that women kind of have to have as being framed as personal expenses/indulgences

Yeah, I was thinking of the pink tax – tampons are a household expense! Admittedly, we have the same set up as the OP, but I’m the higher earner at the moment. If I wasn’t, I’d push to shift all household grocery and toiletry spends to come from the joint account, so the pink tax was covered fairly. I’ve always been up in the air about clothing budgets for the same reason – it’s not my fault I need more items of clothing, that they cost more, and that they fall apart faster than a man’s, so why should I be penalised and pay for that out of my personal expenditure? But if it was joint, then I’d feel so much guiltier about buying clothes on a whim, and it’s nice not having that hanging over me too.

Totally agree, great great points. I’ll have to confront my own guilt issues, but it seems more legit this way.

I’d just like to point out that while this is a great way to ease into sharing, I’m not sure in the long run it’s healthy. I also know people will disagree with me with “but what if you split” etc.

The thing is, incomes rarely are static, and they are also rarely equal. As you mention, one of you earns more than the other. Life is filled with unexpected twists. At some point, I think you have to take a deep breath and decide to go all in or you risk building resentment, jealously, control issues, power imblances or just unhealthy attitudes in your couple.

I say this from the perspective of a seventeen year old couple. When we first were dating, I was a student so he paid more because I was broke as hell. Than I graduated but he was unemployed for six months so the situation reversed. I was in a car crash and without revenue a while a few years later. But a few more years and he had a back injury. Then we had a kid and we chose that I would stay home for a year. I think you get the idea! Anyway, at some point you lose track. And trying to stick each to your own guns despite one person who earns less having to struggle constantly seems a lack of compassion. Unless I mean lack of commitment? Or trust? At some scary point, you just have to decide to let go. And yes, I know that if we seperate I will not be getting some of that money back. And he won’t be getting some of his money back. I believe in our love enough to take that risk.

(If there are important assets, like for a business owner or something then I think a prenup, or some other legal document stating what is protected is absolutely a good idea.)

In our family we also split our money into three pots but in the opposite way – everything goes into one account, then we both draw the same allowance out of this. This gives us the freedom to spend this in different ways without judgement, but means we are both equally well off. This feels really nice to us.

Now that you mention it, that is actually how we work too!

I’m actually totally with you that, ultimately, keeping things “equal” might cause more strife than anything else. But I figure I’ll deal with that once we’re married (we’re not right now), then the legal issues are less sticky than they are now. But, absolutely agree!

I think this can definitely work in the long term as long as the couple reevaluates each time a salary status changes. For example, my husband and I currently split the joint bills 53/47 because that’s the income split of our household. When my pay goes up this July we’ll re-run the numbers, see if the percentages have changed, and if so start paying the new amount from that day forward.

I LOVE seeing a post about this system because it’s sort of like the system my husband and I use and we get so much grief for it. People think that we should just put all our money into a big pot and have it be a free for all and I just can’t. I don’t think I have any right to spend money he earns or vice versa. I don’t want to buy his frozen chicken and I’m sure he doesn’t want to fund my StitchFix!

Our joint account is strictly for household repairs/improvements though. I’m the only one who puts money in it on a consistent basis (10% of each check) so it’s not overflowing with funds! For our joint bills we split them along income percentage lines. I pay the full amount out of my personal account and then he gives me his share in cash which I then use as my spending money.

I think systems like these, a “sometimes share system” I’ve heard them called, are becoming more prevalent as couples wait longer to move in together, get married, start a family, etc. I think it makes the most sense for two people who are used to handling their own finances to use a system like this. It’s sharing responsibility while keeping some independence.

It’s like you’re speaking to my heart! I have financial control issues (stemming from several experiences in my twenties, during which asshole roommates and boyfriends stole about $6K from me)- I’m grateful that my fiance understands this twitch. We have totally separate finances, but a shared credit card (for the points) and we’re equitably splitting all bills, groceries, and dining out (together) expenses. However, it’s been creating a lot of work and pressure for me- so this feels like a good potential solution. We’ll be abandoning the shared credit card idea soon (found out what a waste of effort THAT was- we have tons of airline miles and using is next to impossible thus far), so this three pot idea is an elegant solution. Also, spreadsheets. Yay!

Would you mind sharing more about why you found the shared credit card to be a disaster? We’ve been talking about looking into getting a shared credit card (right now we have a shared checking account and debit cards, but we want to be earning more airline miles, hence wanting a shared credit card), but if you have a cautionary tale that would advise against it, that would be super helpful to hear!

Sure- less of a disaster and more of a stressor. Because I’m the detail-oriented one with the twitch about money, I do all of the checkbook balancing, so I’m having to crunch numbers every week, divide up who paid for what, make sure our entire balance is paid each month by a certain date (which I pay on my account, and then he Paypal reimburses me), etc. The one month I forgot to do that, we racked up a $70 finance charge by not paying the entire balance on time. And then to find out that the entire reason for having a shared credit card (to earn miles, for the honeymoon) was basically null (it was $1K cheaper to buy our tickets outright than to redeem miles and pay the fee for it), made that weekly number crunching feel like a waste of energy (and I have chronic fatigue, so I horde my energy jealously).

I expect, if you already have shared accounts, you won’t have the issue I had, as you’ve already got a system for making things equitable. But in terms of miles, my advice would be to make sure you know exactly which airline serves all the destinations you’re likely to go to. We got an Alaska Air card, because we live in Seattle and it’s an Alaska Air hub. Turns out, Alaska doesn’t really fly past Denver or so, so we haven’t been able to redeem anything thus far (our trips were to Ohio, Virginia, and the upcoming honeymoon to the UK). Also, it’s a card with a yearly fee, which is paying money for nothing we can use. So now I find myself planning trips to Alaska Air destinations solely so we use up those darn miles, which is spending money to save money, and not the smartest move.

That said, cards whose points you can redeem for a multitude of things (including miles) have a lower dollar-to-mile rate, but probably offer more freedom, so may be a better choice. Good luck to you, either way!

I’m a big believer that if it works for you then do it! For us i don’t know how this would work. We each have our own checking accounts and we don’t have a joint account. He’s terrible at saving so our joint savings are in my savings account. As for bills i keep better track of things and we’ve agreed that if left to him we would have many late fees so all the bills come out of my account. He makes a significant amount more than me so he pays the babysitter, and pays for groceries then gives me whatever he’s able to each week. Most weeks this is a decent portion of his check but if he knows he’s gonna be buying something then he keeps the amount he needs for it. He also makes sure to keep money for himself each week for gas, eating out or other personal spending. Toiletries and things for the babies like diapers and wipes come out of the grocery money. We budget together or how much is needed for that every month. This allows him to have the freedom with his own money and decide what he can afford each week. I then allocate that money as needed and put the remainder into savings. In order to be sure we have enough for the bills each month we discuss how much we’ll need and how much of that i can afford to pay. The remainder is his responsibility and if he’s able to put more it’ll go into savings. If either of us wants or needs something that we couldn’t afford to pay with cash on hand we discuss it and if necessary take that from the savings. We have the same bank so we can easily transfer money around if it becomes necessary but that doesn’t happen very often.

I’ve participated in many discussions on how to share household finances over the years and I think the main thing I’ve learned is that there is no “right” way to do it – everyone wants different things for different reasons. I’ve been assured that my marriage is doomed to fail if we can’t trust each other enough to put all our money into one account and then spend whatever we want without keeping track of who earns what and who spends it. I’ve equally been assured that doing that is guaranteed to lead to resentment and we absolutely must keep our money entirely separate and split the bills exactly equally. And that splitting the bills equally is a terrible idea and it needs to be shared out based on what we earn…..and so on.

I’ve come to the conclusion that (like most aspects of family life) the most important thing is that all the people involved are happy with the system THEY have. Learning about how other people do it and why is certainly helpful, but you’ve got to find the system that works for you and not worry about whether anyone else thinks it’s right.

For my husband and I that’s a simplified version of what’s in the original post. We each have our own accounts which our wages go into, then we each pay 2/3 into a join account which we use to pay our bills and other shared expenses. The remaining money we’re free to do whatever we want with. It means my husband is able to spend more than I am, because he earns more, but it also means I don’t stress over every purchase, worrying about what he might have wanted to do with the money or what I can’t have because he’s bought something.